If you read some of the press you’d might think the interest in electric cars has waned. Some of the press, especially from the right (Wall St. Journal, The Hill), are already predicting the failure of EVs. But that’s all mostly political opinion and is more wishful thinking than factual. It’s fostered by their opposition to Biden’s support of EVs and their skepticism of climate change.

The adoption curve of new products is rarely linear. It usually has several inflection points and bumps. We’re now in the Early Adopter phase where growth is still slow. But we’re approaching the transition from Early Adopters to Early Majority where the rate of sales increases.

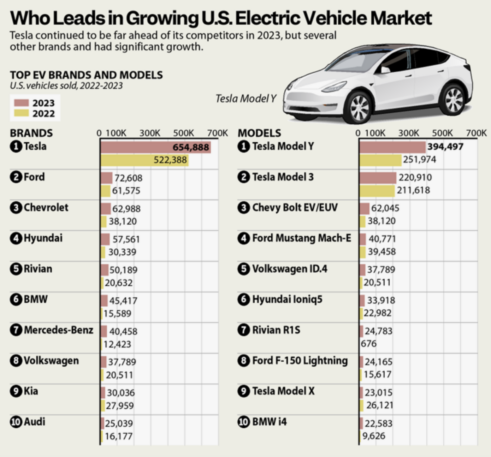

The growth of the market leader Tesla, who once had 100% of the market, is stalling. Tesla unit sales had grown about 50% per year until last year, but in its last quarter sales grew just 20% year-over-year, and some now think the next quarter might be flat or even down.

(I think it could be down, based on Tesla’s messaging. If you look at Tesla’s own statements, they’ve had a cumulative production of 6 million cars to date. Tesla also reported sales of 5.57 million cars from inception as of 12/31/23. If both numbers are accurate, this means Tesla produced just 430,000 cars in Q1’24, down 13% from 495,000 cars in Q4’23. And much of this was over a period where they cut the selling price of some models by 20%.)

Since Teslas has such a large market share, the slowdown in their sales contributes to a major reduction in EV sales growth, and masks some of the large increases experienced by many of the new entrants. BMW for example grew its EV sales by 48% year over year.

Slowing sales at Tesla are the result of a number of factors that have nothing to do with interest in EVs. Tesla CEO Elon Musk has alienating millions with his bizarre behavior, admitted drug use, and support of right wing and Nazi causes, turning off many potential buyers. See graph below.

Secondly, Teslas have not changed in their basic design in over eight years, something no normal car company could tolerate. While hugely innovative eight years ago, they look much the same today and the interiors are sparse and barren and they have fewer convenience and comfort features compared to many of the new entries. As for his Cybertruck, that’s more of a vanity project that’s not of interest to most car buyers. Tesla may be about to begin a tailspin, much of it self-inflicted. Could they be the Blackberry of smartphones?

The other contributions to slower sales are the stumbles GM and Ford have made with their EV strategy. GM in particular first canceled and then restarted the Chevy Bolt, one of the best selling, least expensive EVs. Then they stumbled with the introduction of the Chevy Equinox that had catastrophic quality issues with its electronics. Ford in their exuberance, overpriced some of their models and are now making corrections across the board. More competitive pricing should be a positive effect.

The consensus among automotive analysists is that there will be good overall growth this year following a strong 2023 with 1.19 million all-electric cars sold, up 46% from the prior year, according to Cox Automotive. “EV sales are increasing faster than any other segment in the industry,” said Michelle Krebs, executive auto analyst for Cox. 2024 looks to be a strong year with EV sales expected to be 10% of car sales.

There are now about twenty manufacturers of EVs, most of whom are bringing out multiple models with a wide variety of body styles to offer something for everyone. There’s even a new 3-seat SUV from Kia that’s heavily backordered. The choices of body styles, prices, and features have never been as broad as they are today.

Like most new products, initial models are premium priced to gain sales from early adopters willing to pay more to be first. As new models arrive, competition increases, prices drop, and new lower cost models are introduced. The cycle is predictable and happens with all consumer products where there are multiple players.

The adoption curve for EVs is following the same curve we had for large screen flat TVs, where the display panels can be compared to car batteries. Each constitute the largest cost element in their respective product and both costs drop through manufacturing efficiencies and technical advances. The only variable is the time scale on the adoption curve. Some adoptions can take a year or two while others span more than a decade.

Initially a 50-inch plasma TV cost $5000 for a couple of years, then began to drop in year 3 to $2500 for LED TVs. As new manufacturers and cheaper technology came on line, we see prices now as low as $400 for even better performing sets. The same is beginning to happen with battery technology.

Inherently, an EV is a vastly simpler car to manufacture and much less expensive to own than a gasoline powered one. As the cost of batteries fall, we will eventually see EVs costing significantly less than internal combustion engines cars.

A lot has been written in the press attributing slow sales being caused by a lack of a widespread charging infrastructure. That has created fears among the public, but much of that is unwarranted, since nearly 90% always charge their cars on a home charger. To counter that concern, some car companies are offering a free loaner car for long trips to alay any fears.

The shift to electric vehicles will continue with a few bumps, but there is little question that EVs will become the largest serment of the automotive industry. The only question how long it will take.